Incorporated in 1970, SRF Ltd manufactures and sells technical textiles, chemicals, packaging films, aluminum foils, and other polymers

Financial Results:

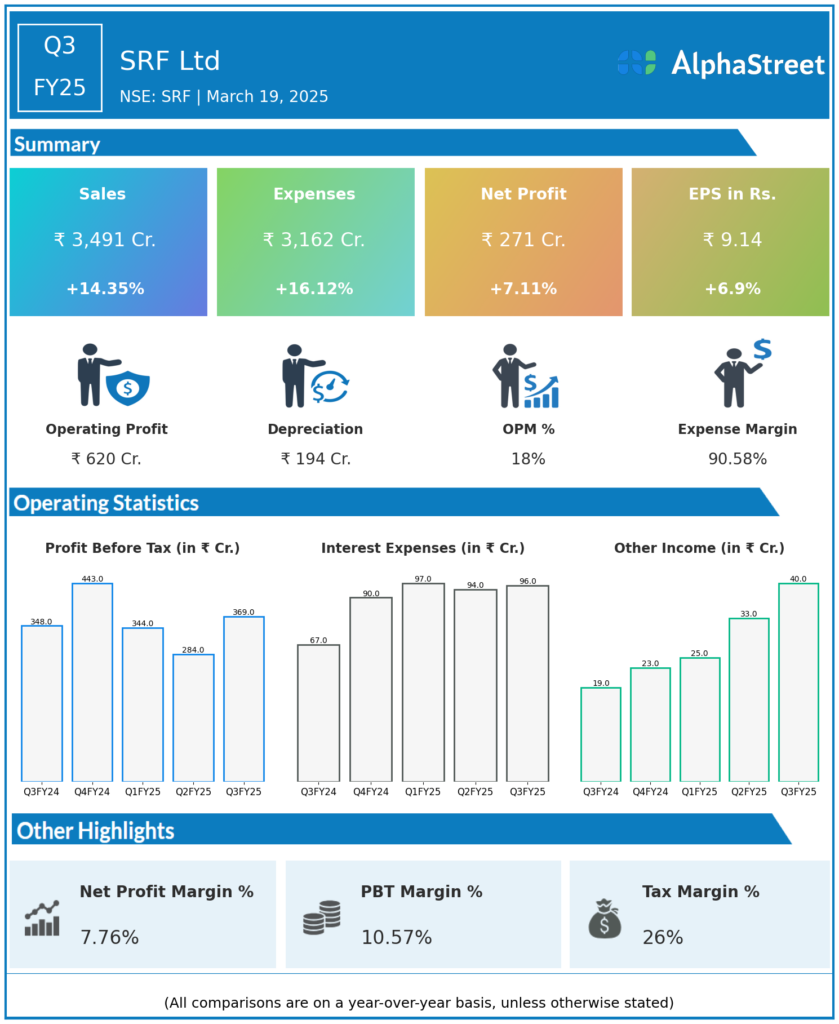

SRF Ltd reported Revenues for Q3FY25 of ₹3,491.00 Crores up from ₹3,053.00 Crore year on year, a rise of 14.35%.

Total Expenses for Q3FY25 of ₹3,162.00 Crores up from ₹2,723.00 Crores year on year, a rise of 16.12%.

Consolidated Net Profit of ₹271.00 Crores up 7.11% from ₹253.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹9.14, up 6.90% from ₹8.55 in the same quarter of the previous year.