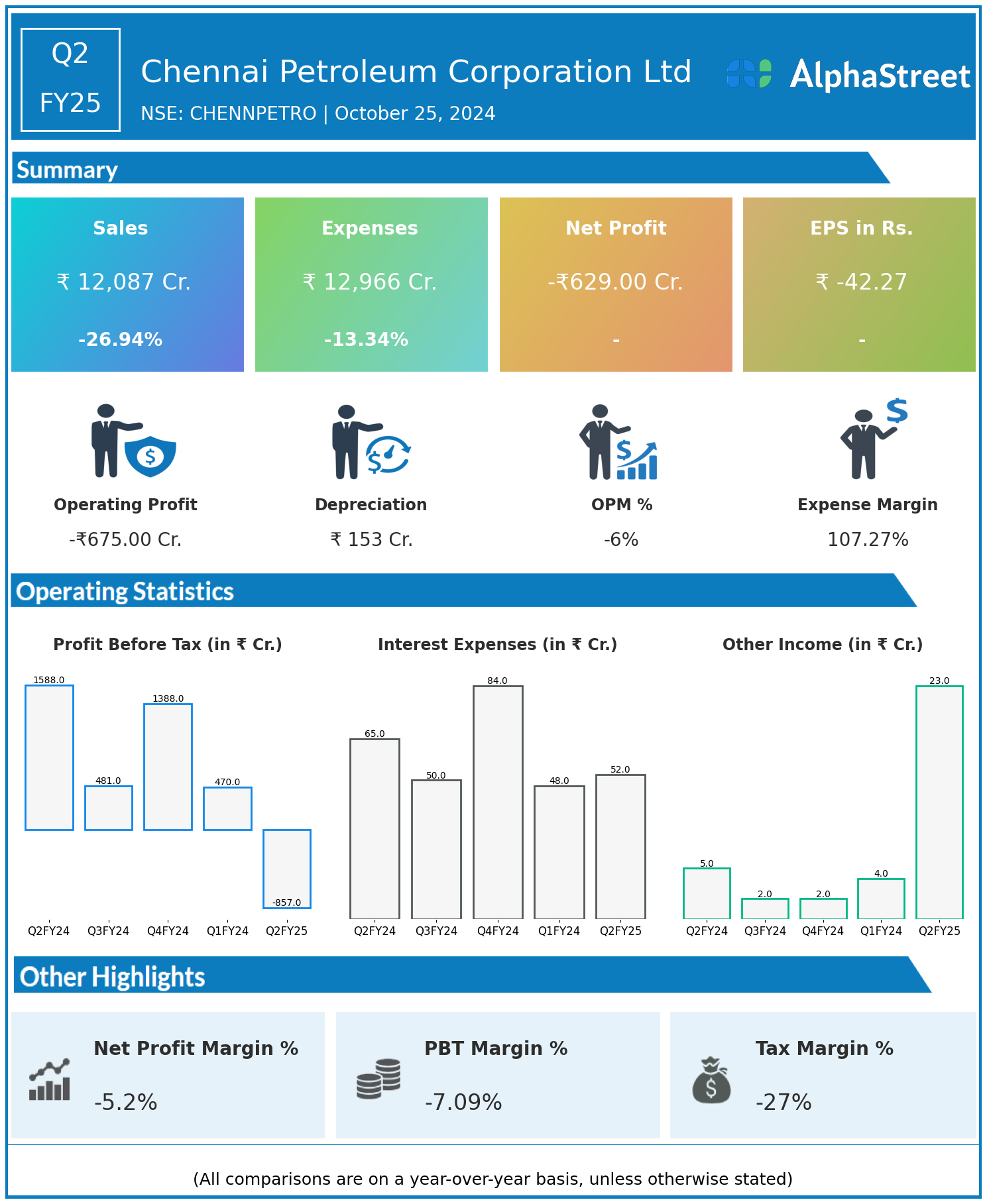

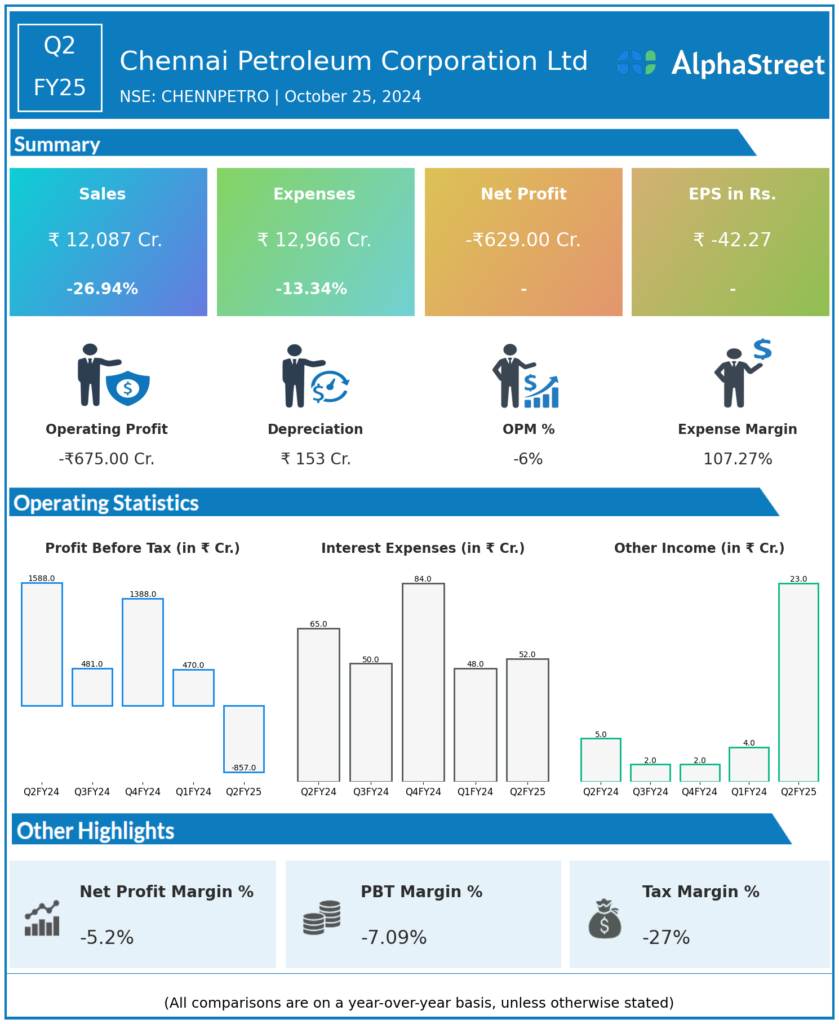

Chennai Petroleum Corporation Limited is in the business of refining crude oil to produce & supply various petroleum products and manufacture and sale of lubricating oil additives.

Financial Results:

Chennai Petroleum Corporation Ltd reported Revenues for Q2FY25 of ₹12,087.00 Crores down from ₹16,545.00 Crore year on year, a fall of 26.94%.

Total Expenses for Q2FY25 of ₹12,966.00 Crores down from ₹14,962.00 Crores year on year, a fall of 13.34%.

Consolidated Net Profit of -₹629.00 Crores from ₹1,191.00 Crores in the same quarter of the previous year.

The Earnings per Share is -₹42.27, from ₹79.95 in the same quarter of the previous year.