Dixon Technologies (India) Limited is the largest* home grown design-focused and solutions company engaged in manufacturing products in the consumer durables, lighting and mobile phones/smart phones markets in India. Their diversified product portfolio includes (i) consumer electronics like LED TVs; (ii) home appliances like washing machines; (iii) lighting products like LED bulbs and tubelights, downlighters; (iv)mobile phones/smart phones; and (v) CCTV & DVRS (vi) Medical Equipment. Dixon also provides solutions in reverse logistics i.e. repair and refurbishment services of set top boxes, mobile phones /smart phones and LED TV panels.

Financial Results:

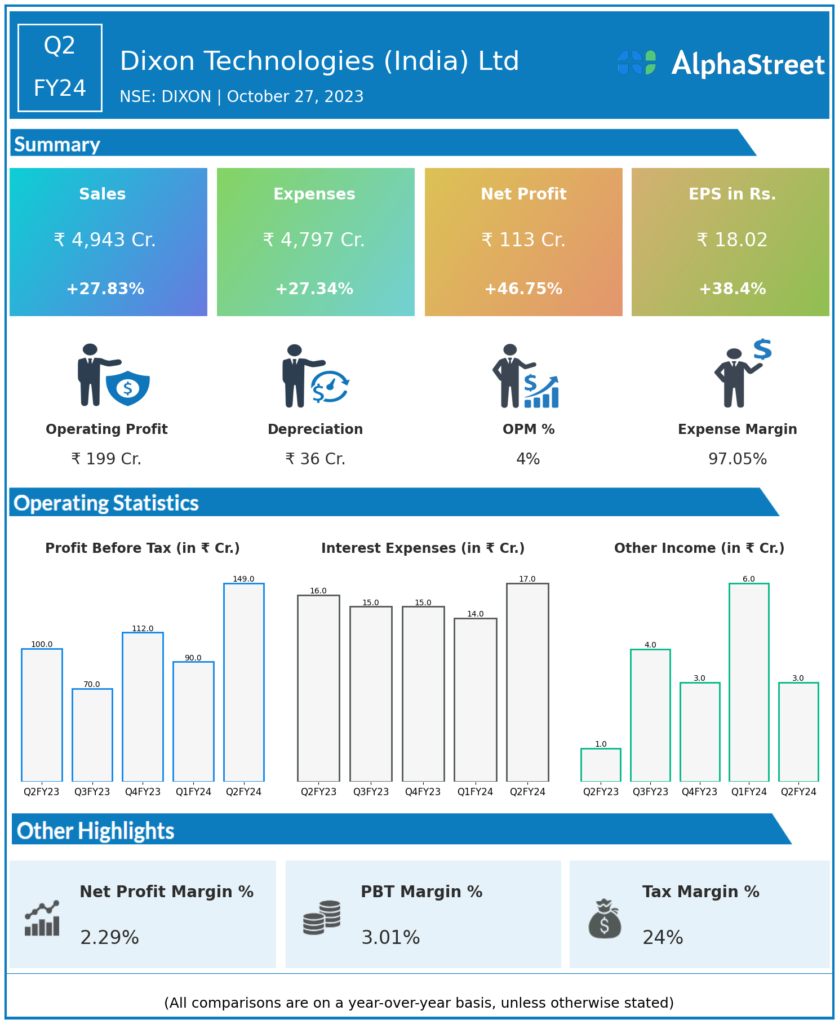

Dixon Technologies (India) Ltd reported Revenues for Q2FY24 of ₹4,943.00 Crores up from ₹3,867.00 Crore year on year, a rise of 27.83%.

Total Expenses for Q2FY24 of ₹4,797.00 Crores up from ₹3,767.00 Crores year on year, a rise of 27.34%.

Consolidated Net Profit of ₹113.00 Crores up 46.75% from ₹77.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹18.02, up 38.40% from ₹13.02 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.