ESAB India Ltd is a leading supplier of welding and cutting products in India. It is a subsidiary of ESAB Group which was ultimately owned by the Colfax Corporation of USA.

Financial Results:

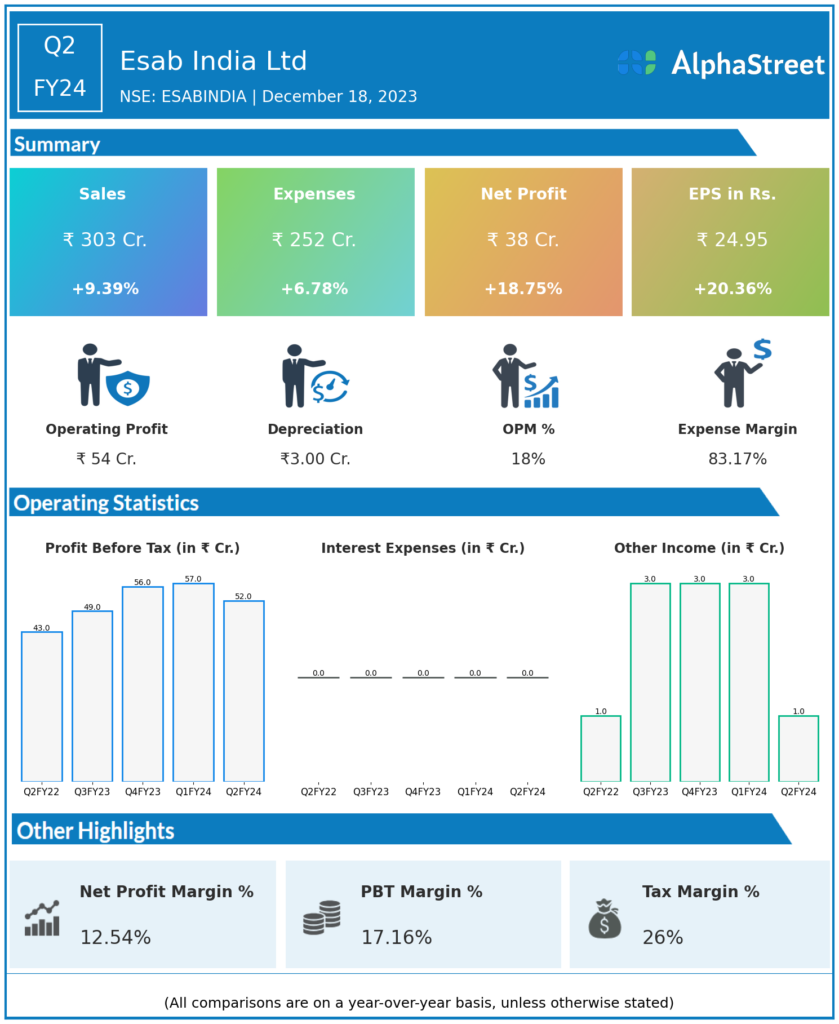

Esab India Ltd reported Revenues for Q2FY24 of ₹303.00 Crores up from ₹277.00 Crore year on year, a rise of 9.39%.

Total Expenses for Q2FY24 of ₹252.00 Crores up from ₹236.00 Crores year on year, a rise of 6.78%.

Consolidated Net Profit of ₹38.00 Crores up 18.75% from ₹32.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹24.95, up 20.36% from ₹20.73 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.