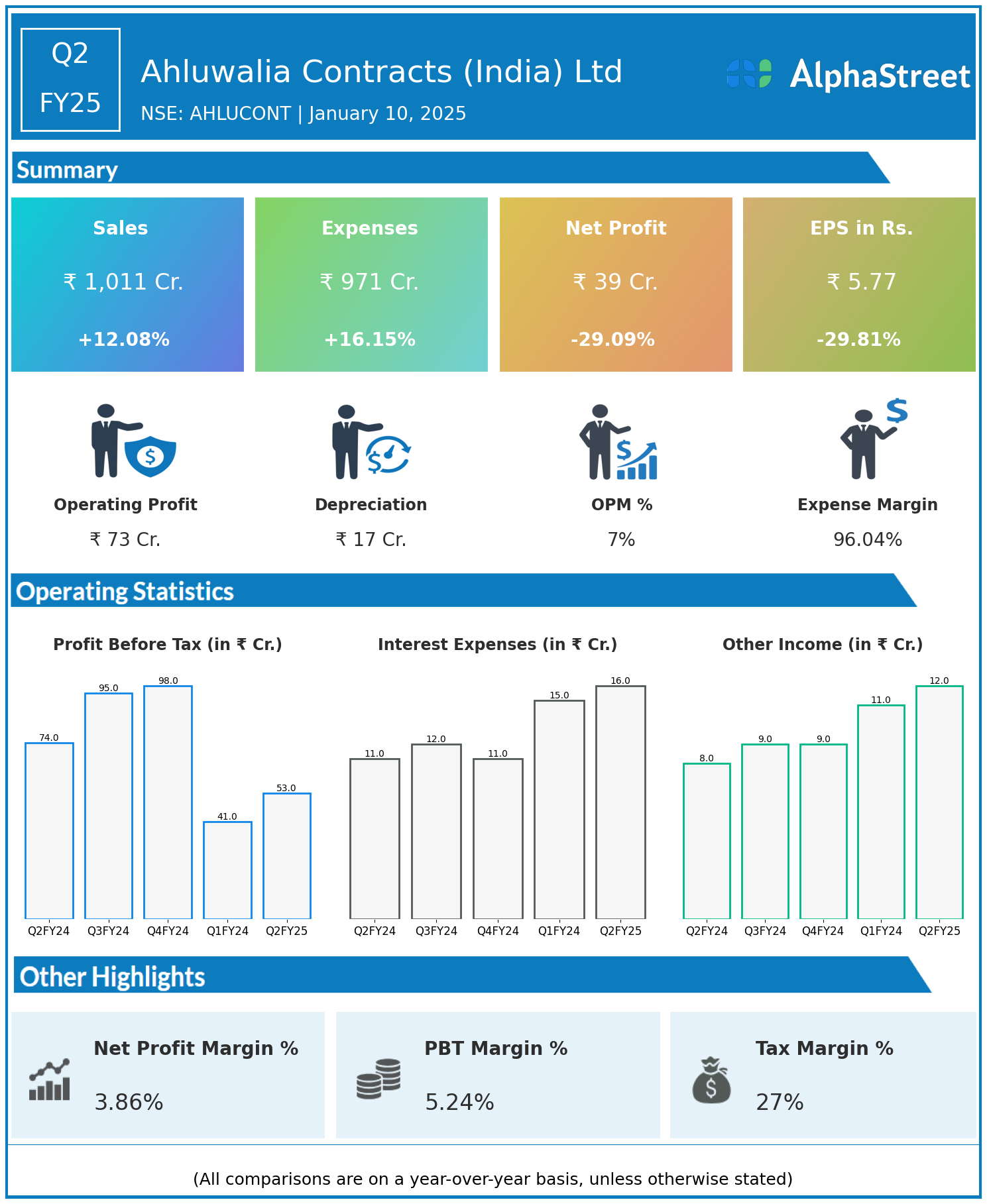

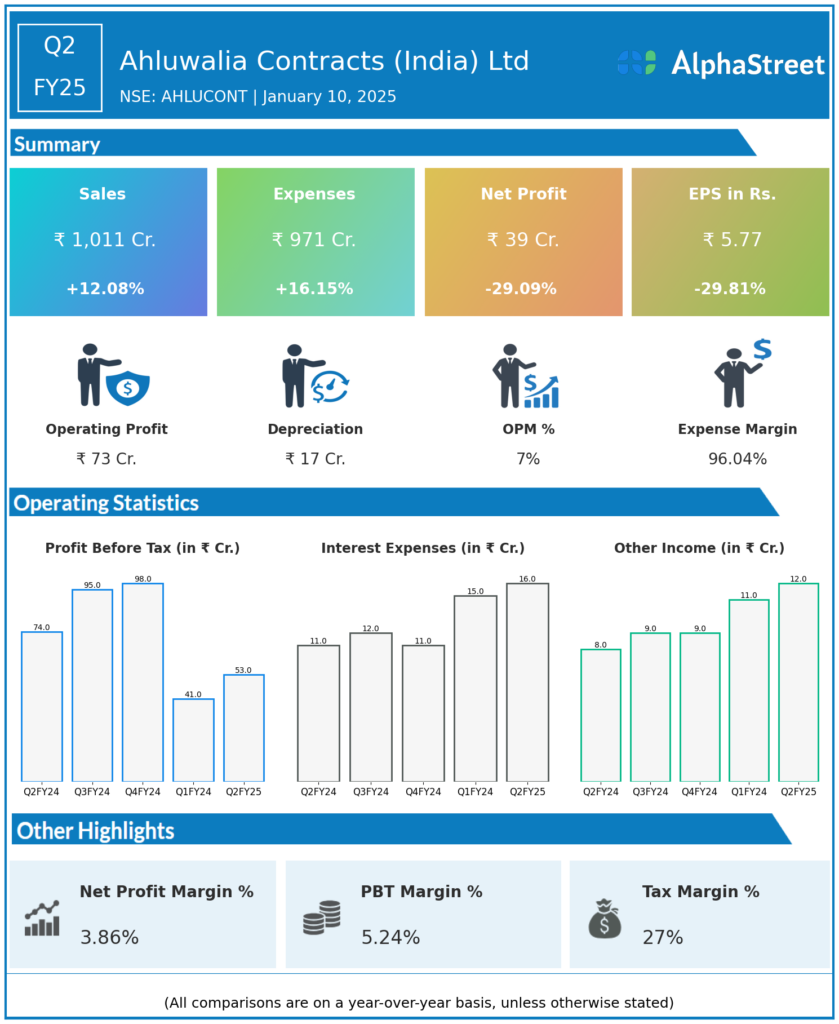

Company is engaged in engineering and contract construction, delivering state of-the-art infrastructure and buildings projects for clients in India.

Financial Results:

Ahluwalia Contracts (India) Ltd reported Revenues for Q2FY25 of ₹1,011.00 Crores up from ₹902.00 Crore year on year, a rise of 12.08%.

Total Expenses for Q2FY25 of ₹971.00 Crores up from ₹836.00 Crores year on year, a rise of 16.15%.

Consolidated Net Profit of ₹39.00 Crores down 29.09% from ₹55.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹5.77, down 29.81% from ₹8.22 in the same quarter of the previous year.