Aarti Industries Ltd, the flagship company of the Aarti group, manufacturing organic and inorganic chemicals at its major facilities in Vapi, Jhagadia, Dahej and Kutch, in Gujarat and in Tarapur in Maharashtra. The company has a strong market position in the NCB-based specialty chemicals segment.

Financial Results:

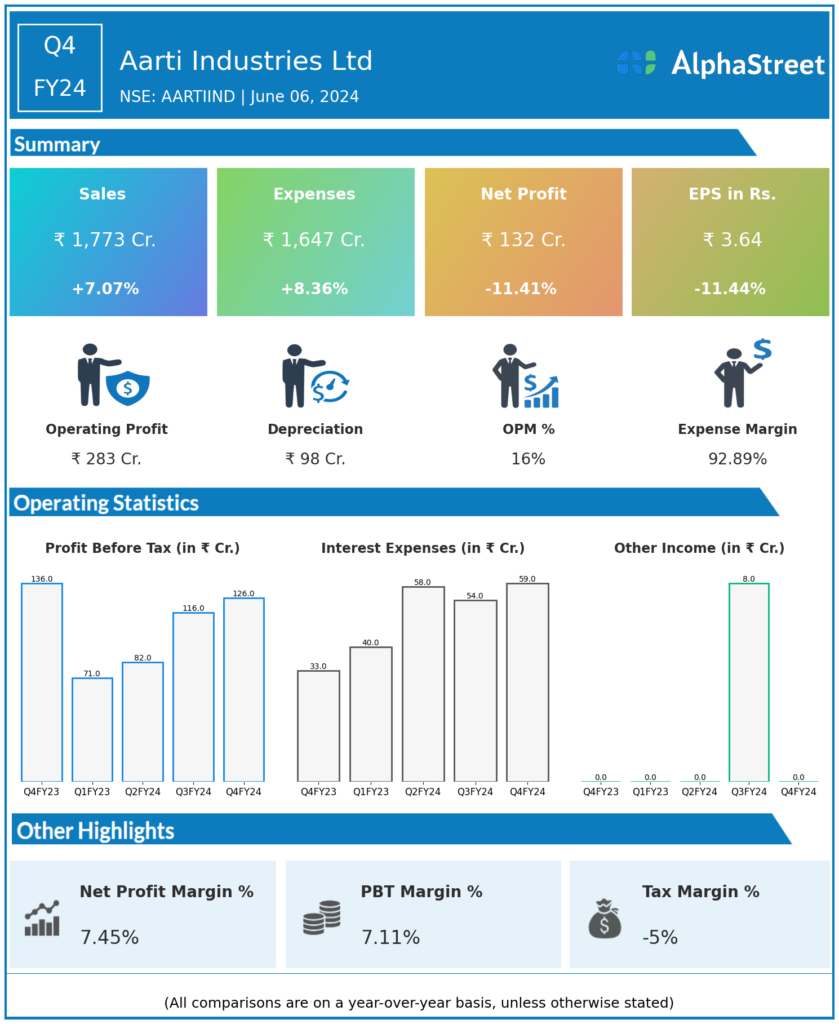

Aarti Industries Ltd reported Revenues for Q4FY24 of ₹1,773.00 Crores up from ₹1,656.00 Crore year on year, a rise of 7.07%.

Total Expenses for Q4FY24 of ₹1,647.00 Crores up from ₹1,520.00 Crores year on year, a rise of 8.36%.

Consolidated Net Profit of ₹132.00 Crores down 11.41% from ₹149.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹3.64, down 11.44% from ₹4.11 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.