VRL Logistics is engaged in logistics services dealing mainly in domestic transportation of goods. Other businesses include bus operations, transport of passengers by air, sale of power and sale of certified emission reductions (CER) units generated from operation of wind mills. The operations of the Company are spread all over the country through various branches and transshipment hubs.

Financial Results:

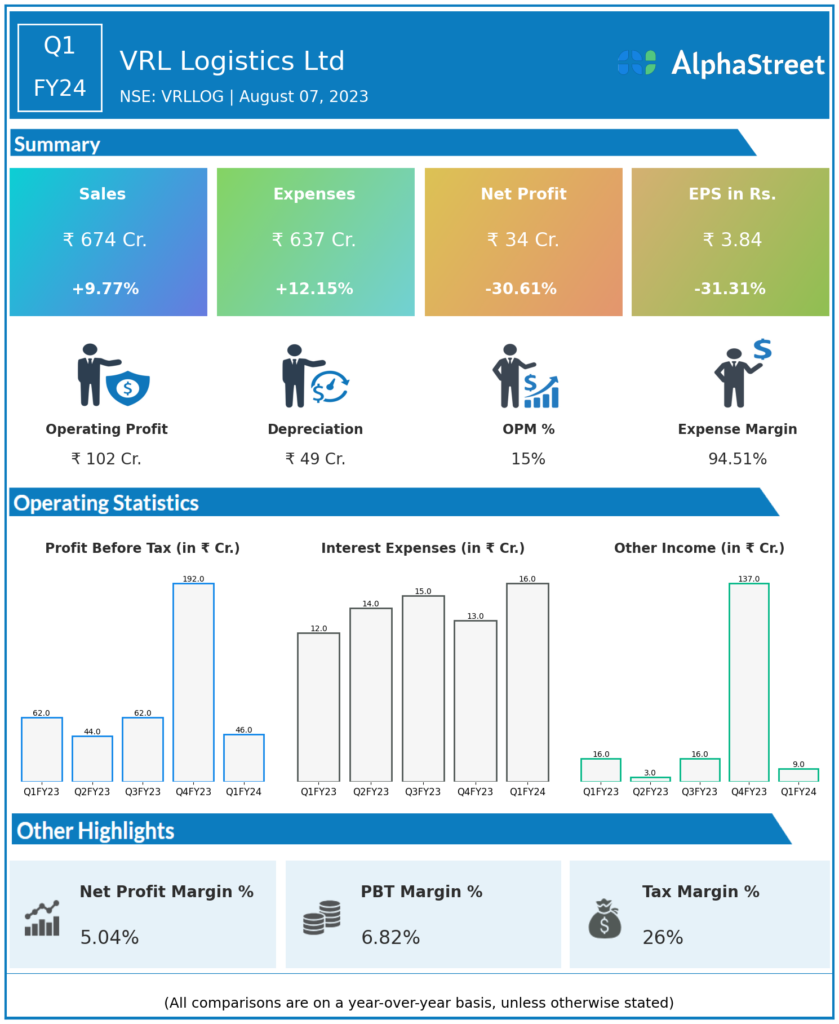

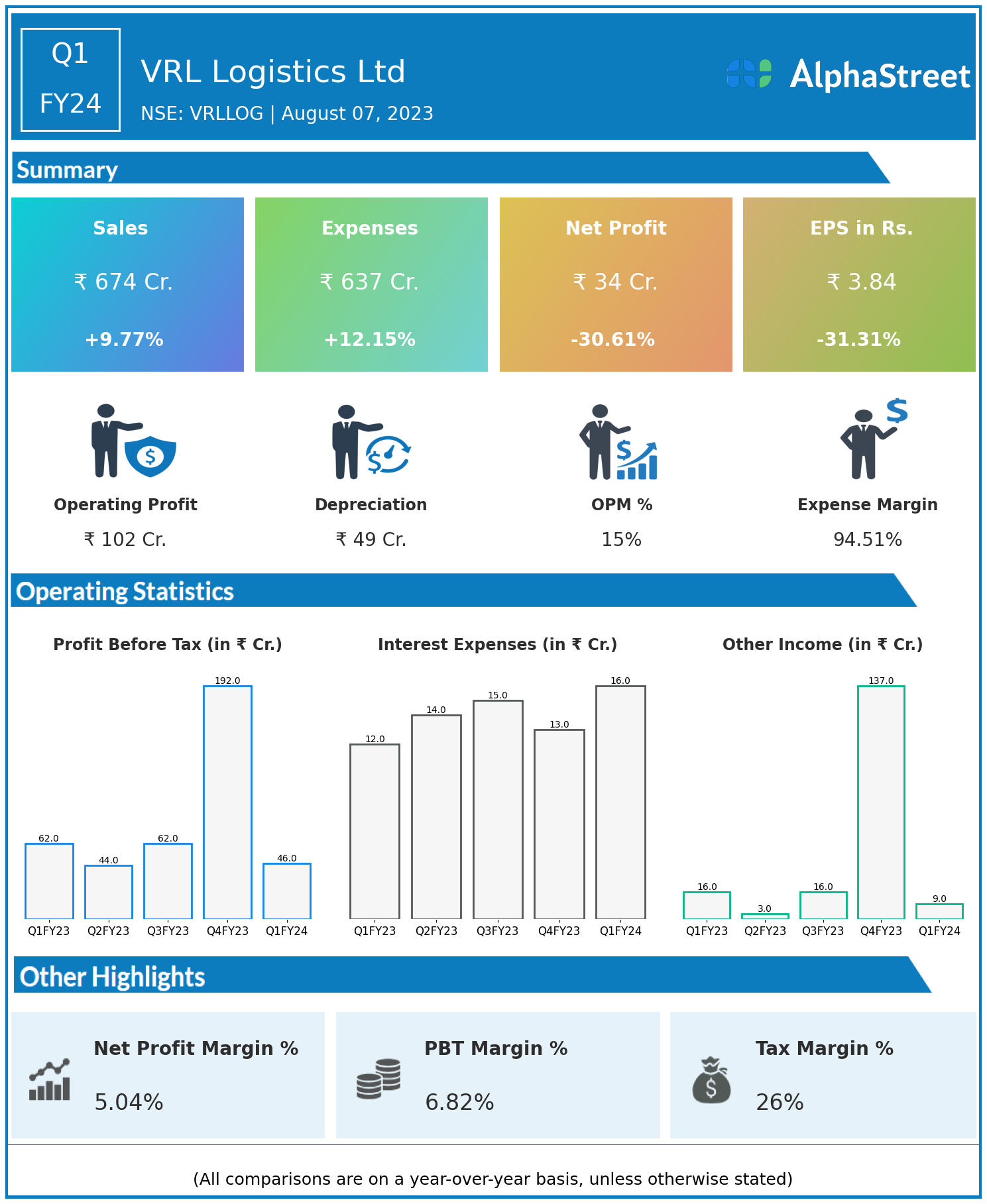

VRL Logistics Ltd reported Revenues for Q1FY24 of ₹674.00 Crores up from ₹614.00 Crore year on year, a rise of 9.77%.

Total Expenses for Q1FY24 of ₹637.00 Crores up from ₹568.00 Crores year on year, a rise of 12.15%.

Consolidated Net Profit of ₹34.00 Crores down 30.61% from ₹49.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹3.84, down 31.31% from ₹5.59 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.