India Cements Ltd., (NSE:INDIACEM), a subsidiary of UltraTech Cement Limited, stands as a prominent regional leader in South India undergoing a significant operational turnaround and strategic transformation following its acquisition by UltraTech Cement Limited in December 2024.

Competitive Context

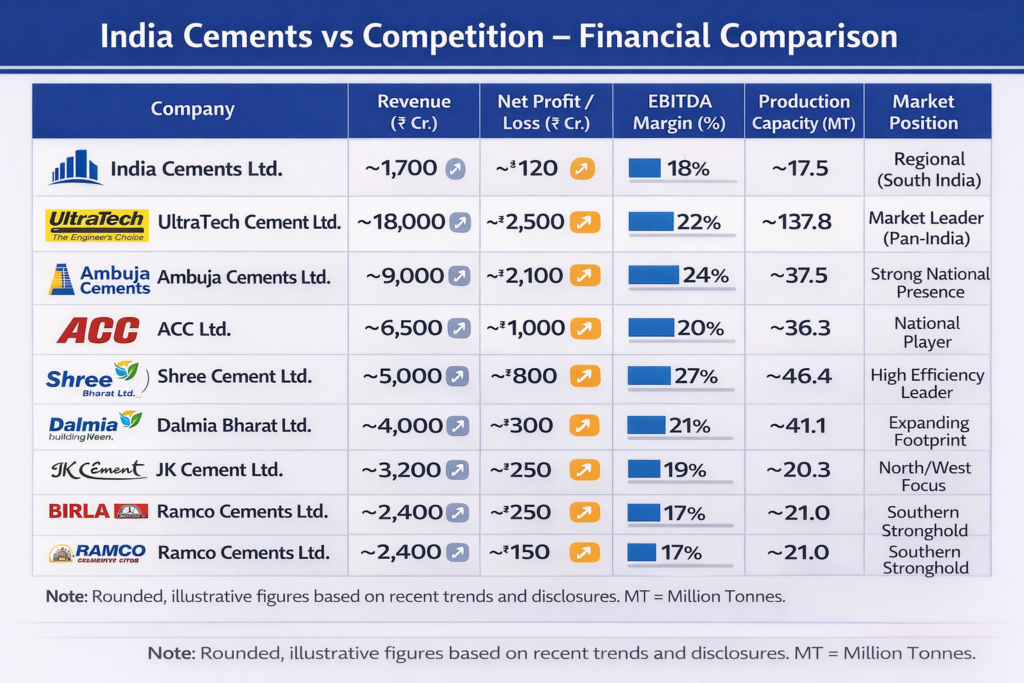

The top cement makers together control a large share of the Indian market, reflecting industry consolidation and scale-based rivalry. India Cements competes not just on production capacity but also on regional strength, especially in South India and distribution network.

Major National Competitors

These are the biggest rivals in terms of market share, scale, and industry impact:

- Ambuja Cements Ltd. : Part of the Adani Group, a major national player with extensive manufacturing and distribution.

- ACC Ltd. : Also owned by the Adani Group and a well-established cement brand competing nationwide.

- Shree Cement Ltd. : Among India’s top producers with strong operational efficiency and presence in North/East India.

- Dalmia Bharat Ltd. : A major diversified cement company with good regional coverage and product mix.

Other Notable Competitors

Smaller but relevant companies that compete regionally or in niche segments:

- The Ramco Cements Ltd. : Significant in the southern market with a strong regional footprint.

- Birla Corporation Ltd.: Active player with a presence across central and western India.

- JK Cement Ltd.: Known for both grey and white cement products, with northern/western reach.

- Orient Cement Ltd.: Smaller regional cement maker with presence in several states.

- HeidelbergCement India Ltd.: Indian arm of global group HeidelbergCement, also competing in select markets.

Brand Competition

- India Cements competes in the marketplace through its established brands: Sankar, Coromandel, and Raasi. These brands face direct pricing and quality competition from products like Birla Cement, Jaypee Cement, and Banger Cement.

Consolidation and Strategic Ownership

- The industry is in an advanced phase of consolidation, with the top five players now controlling approximately 62% of the market share, up from 45% in FY19. India Cements is a central figure in this trend, having become a subsidiary of UltraTech Cement Limited in December 2024.

Industry Trends and Demand

- The broader market is experiencing a demand upcycle driven by significant government infrastructure spending (₹11.11 trillion capex for FY26) and housing initiatives like the Pradhan Mantri Awas Yojana (PMAY).

Operational Shifts

- Regional players are facing a shift toward industrialized concrete production (RMC) and a growing dominance of blended cements (PPC and PSC), which now account for nearly 65–70% of total usage in India.

Sustainability Imperatives

- In line with India’s goal of Net-Zero CO₂ by 2070, the industry is aggressively transitioning to green energy, with India Cements specifically targeting a 80% Green Power mix by FY29 through investments in Waste Heat Recovery Systems (WHRS) and solar power.

Stock Performance

- Ownership Transition: The company’s stock value has been heavily influenced by its strategic transition; UltraTech completed the purchase of an additional 32.72% stake for approximately $460 million in late 2024, bringing its total shareholding to 55.49%.

- Current Results: The company demonstrated a financial rebound in Q3 FY26, reporting a Profit After Tax (PAT) of ₹6 Crores before exceptional items and a positive consolidated EBITDA of ₹103 Crores, reversing a loss of ₹178 Crores from the previous year.

Summary

UltraTech Cement dominates in scale, revenue, and profitability. Ambuja & ACC benefit from Adani Group integration and cost efficiencies. Shree Cement leads in operational efficiency and margins, while India Cements shows improving profitability, margin recovery and strong regional presence. Competition remains intense due to capacity expansion and pricing pressure.