EIH is primarily engaged in owning and managing premium luxury hotels and cruisers under the luxury Oberoi, Trident and Maidens brands. The Company is also engaged in flight catering, airport restaurants, project management and corporate air charters.(Source : 202003 Annual Report Page No:124)

Financial Results:

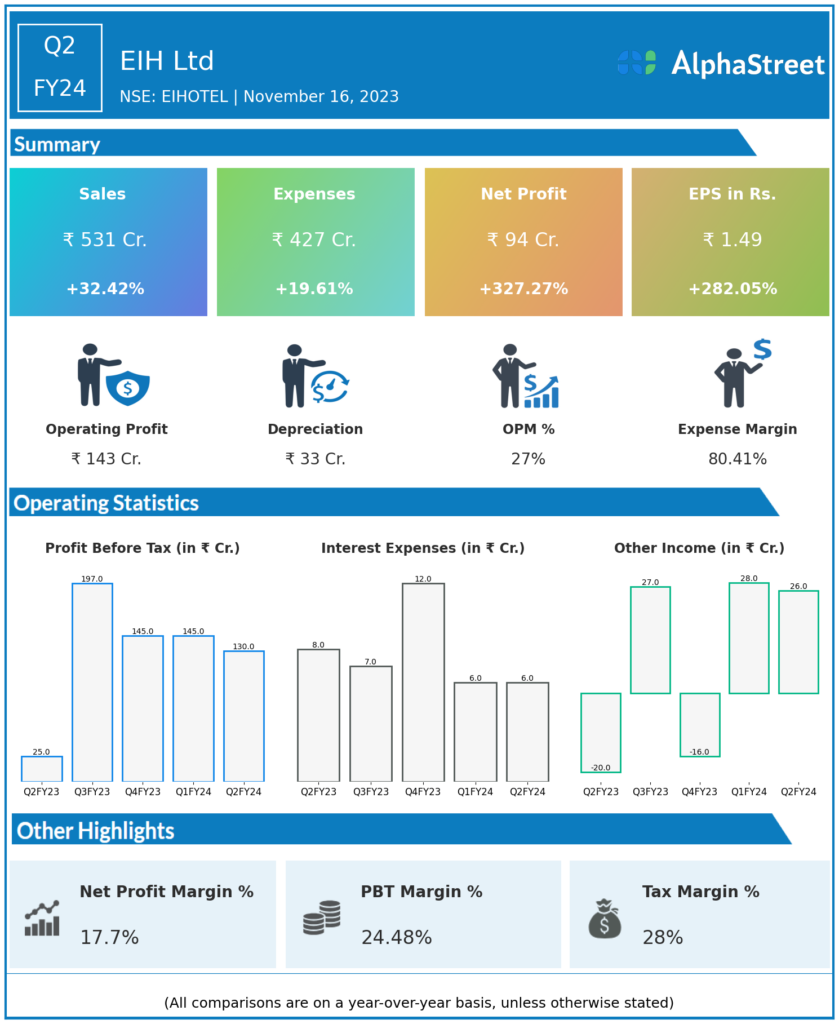

EIH Ltd reported Revenues for Q2FY24 of ₹531.00 Crores up from ₹401.00 Crore year on year, a rise of 32.42%.

Total Expenses for Q2FY24 of ₹427.00 Crores up from ₹357.00 Crores year on year, a rise of 19.61%.

Consolidated Net Profit of ₹94.00 Crores up 327.27% from ₹22.00 Crores in the same quarter of the previous year.

The Earnings per Share is ₹1.49, up 282.05% from ₹0.39 in the same quarter of the previous year.

*It is important to note that the way the results have been accounted for are slightly different than the ones the companies may choose to publish.

*The presented data is automatically generated. It may occasionally generate incorrect information.