Talbros Automotive Components is engaged in the business of manufacturing Gaskets and forging. The company is a single source supplier to 5 customers including Hero Motocorp and Bajaj Auto. Other clients include Tata Motors, JLR, HMSI, Volvo, Hyundai, KIA and Maruti

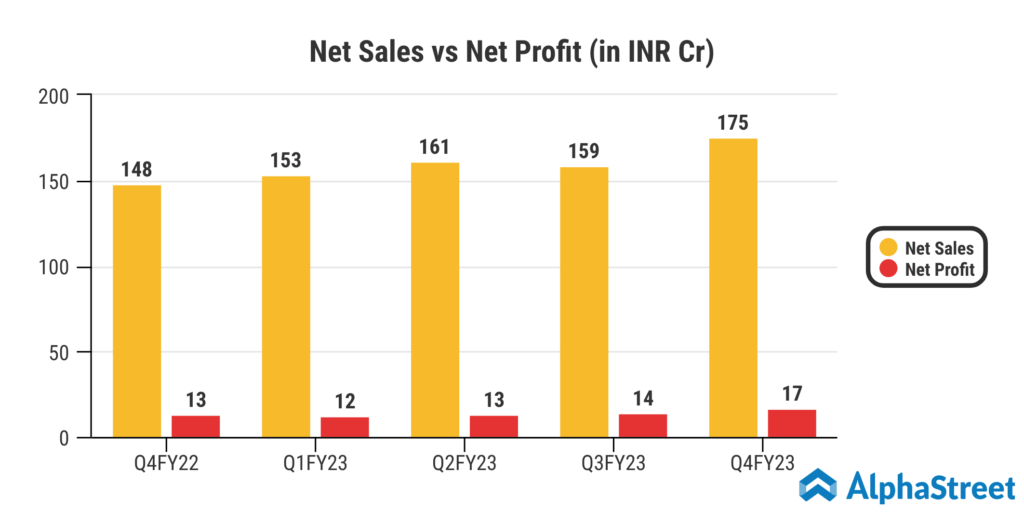

- Talbros Automotive Components Ltd reported Total revenue for Q4 FY23 of ₹175 Crore, up from ₹148 Crore year on year depicting a growth of 19%.

- Total Expenses for Q4 FY23 of ₹159 Crore up, from ₹136 Crore year on year, a growth of 17%.

- Consolidated Net Profit of ₹17 Crore, up 31% from ₹13 Crore in the same quarter of the previous year.

- The Earnings per Share is ₹13.68, up 34% from ₹10.21 in the same quarter of the previous year.